Most Americans insure their cars, their homes, and even their pets — yet far too many overlook one of the most financially devastating risks they face: losing the ability to work. Studies consistently show that a significant portion of the workforce will experience a disabling illness or injury before retirement, yet disability insurance coverage remains one of the most misunderstood and underutilized protections available. Without a paycheck, even the most carefully built financial plan can unravel quickly. At Akston Insurance, we believe informed consumers make better decisions. That’s why this guide breaks down exactly what disability insurance covers, how policies work, and what to look for when choosing the right plan for your needs.

What Is Disability Insurance Coverage?

Most people insure their homes, their cars, and their health — but many overlook one of their most valuable assets: their ability to earn an income. Disability insurance coverage is designed to protect that income. If you become unable to work due to a serious illness or injury, this type of policy steps in and replaces a portion of your lost earnings so you can continue to meet your financial obligations.

In most cases, a disability insurance policy will pay between 60% and 70% of your pre-disability income. While that may not fully replace your paycheck, it can mean the difference between staying financially stable and falling behind on your mortgage, rent, or everyday living expenses.

It is important to understand what disability insurance is not. It is not the same as workers’ compensation, which only covers injuries or illnesses that happen as a direct result of your job. Disability insurance covers you whether your condition is work-related or not. It is also not health insurance — it does not pay for your medical bills. Instead, it replaces the income you lose while you are recovering and unable to work.

There are two main categories of disability insurance to be aware of:

- Short-term disability insurance: Typically covers a portion of your income for a few weeks up to one year, depending on the policy.

- Long-term disability insurance: Kicks in after short-term benefits end and can provide income replacement for several years — or even until retirement age.

At Akston Insurance, we believe understanding the basics is the first step toward making informed decisions about protecting your financial future.

The Real Risk of Disability: Why This Coverage Matters More Than You Think

Here’s a question most people never think to ask themselves: what would happen to your finances if you couldn’t work for nearly three years? If your answer involves a vague plan involving savings, family support, or simply crossing your fingers, you’re not alone — but you may want to reconsider.

The truth is, disability is far more common than most of us assume. According to the Social Security Administration, 1 in 4 twenty-year-olds will experience a disabling condition before they reach retirement age. That’s not a small or fringe risk — those are odds that should make any working adult pause. Yet disability insurance consistently ranks among the most overlooked forms of financial protection available.

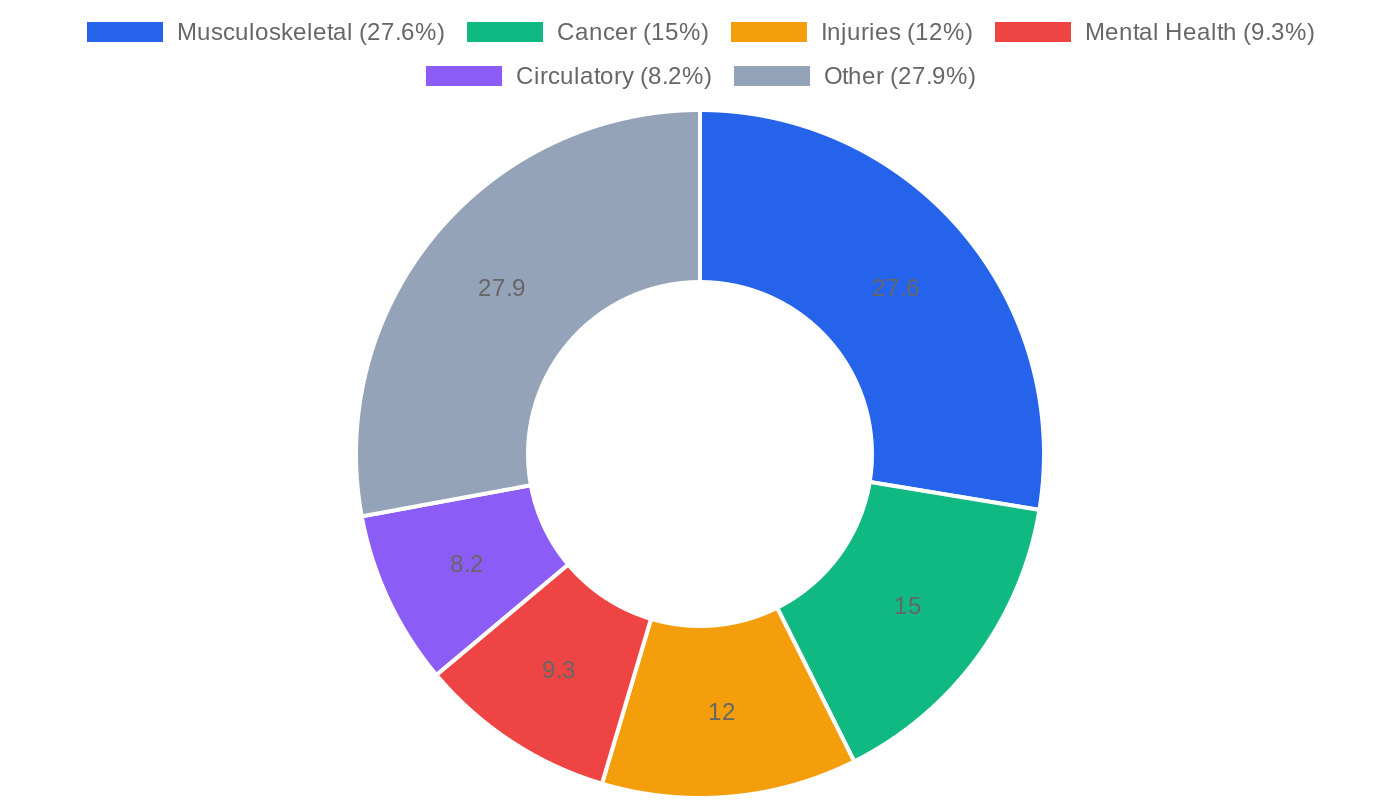

Part of the problem is that people tend to picture disability as something dramatic — a catastrophic accident on a construction site or a sudden traumatic injury. In reality, the data tells a very different story. The majority of long-term disability claims stem from illnesses, not accidents. Conditions like:

- Chronic back pain and musculoskeletal disorders

- Cancer and related treatments

- Heart disease and cardiovascular conditions

- Mental health conditions, including depression and anxiety

…are among the leading culprits. These are everyday health challenges that can affect virtually anyone, regardless of occupation or lifestyle.

What makes this even more sobering is the duration involved. The Council for Disability Awareness reports that the average long-term disability claim lasts approximately 34.6 months — nearly three full years of lost income. For most households, that’s a financial gap that savings alone simply cannot bridge.

At Akston Insurance, we believe that understanding the actual risk landscape is the first step toward making smart, informed coverage decisions. Disability insurance isn’t a niche product for high-risk workers — it’s a foundational tool for protecting your income and your future.

Short-Term vs. Long-Term Disability Insurance: Key Differences

When evaluating your disability insurance coverage options, understanding the distinction between short-term and long-term policies is essential. Both serve a critical purpose, but they are designed to protect you during different phases of a disabling illness or injury. Knowing how each works — and how they interact — can help you build a more complete financial safety net.

| Feature | Short-Term Disability | Long-Term Disability |

|---|---|---|

| Benefit Period | Typically 3 to 6 months | Several months to many years, or until retirement age |

| Elimination Period | Short waiting period, usually 0 to 14 days | Longer waiting period, commonly 60 to 180 days |

| Common Source | Often provided or subsidized by employers | Available through employers or purchased individually |

| Income Replacement | Typically replaces 60–70% of pre-disability income | Generally replaces 50–70% of income over the long term |

| Best For | Short recoveries, temporary injuries, or surgery | Serious illness, chronic conditions, or permanent impairment |

Short-term disability policies are especially valuable when you face a temporary setback — such as recovering from a procedure or a minor injury — and need income support while you heal. Long-term disability coverage, on the other hand, becomes critical when a serious condition prevents you from working for an extended period. Without it, a prolonged illness or permanent impairment could have devastating financial consequences.

Importantly, these two types of policies are designed to complement each other. Many individuals use short-term coverage to bridge the gap during the elimination period of their long-term policy, creating a seamless layer of protection. To learn more about how disability insurance benefits protect your income, the team at Akston Insurance is here to help you evaluate your options and find coverage that fits your unique situation.

What Disability Insurance Coverage Actually Pays For

One of the most common misconceptions about disability insurance coverage is that it helps pay your medical bills. In reality, that’s your health insurance’s role. Disability insurance serves a fundamentally different — and equally critical — purpose: it replaces a portion of your income when an illness or injury prevents you from working. Think of it as a paycheck protection plan for your most valuable asset, your ability to earn a living.

When you receive disability benefits, that money is yours to use however your household needs it most. Most policyholders use their benefit payments to cover everyday essentials, including:

- Mortgage or rent payments

- Groceries and household supplies

- Utility bills such as electricity, gas, and water

- Childcare and family expenses

- Student loan or auto loan payments

- General everyday living expenses

Because disability insurance coverage replaces income rather than reimbursing specific costs, it gives you the financial flexibility to prioritize what matters most during a difficult time.

Beyond basic income replacement, many policies offer optional riders that can enhance your protection. A cost-of-living adjustment (COLA) rider increases your benefit over time to keep pace with inflation. A partial disability benefit rider provides payments if you can return to work in a limited capacity but still experience a loss of income.

Perhaps the most important detail to understand when evaluating any disability policy is how “disability” itself is defined. An own-occupation policy pays benefits if you cannot perform the specific duties of your current profession — even if you could technically work in another field. An any-occupation policy only pays if you are unable to work in virtually any capacity. This distinction can significantly impact when and whether you receive benefits, making it one of the first questions the team at Akston Insurance recommends reviewing carefully before selecting a plan.

Key Terms in Your Disability Insurance Policy (And Why They Matter)

Disability insurance policies can feel like they’re written in a foreign language. But understanding a handful of core terms can make all the difference when you’re comparing coverage options — or, more importantly, when you actually need to file a claim. Here’s a plain-language breakdown of the terms you’ll encounter most often.

Elimination Period

Think of the elimination period as your waiting period — the amount of time you must be disabled before your benefits kick in. Common elimination periods are 30, 60, 90, or 180 days. A longer elimination period generally means lower premiums, but it also means you’ll need sufficient savings or other resources to cover expenses during that gap. Before choosing a policy, ask yourself honestly how long you could manage financially without an income.

Benefit Period

Once your benefits begin, the benefit period defines how long those payments will continue. Options typically range from 2 years or 5 years to longer-term coverage lasting until age 65 or age 67. A short benefit period may be enough for a temporary injury, but a serious illness or chronic condition could leave you unprotected if your coverage runs out too soon. Longer benefit periods offer more security, especially for younger workers with many earning years ahead.

Benefit Amount

This is the monthly payment you’d receive if you became disabled. Most policies are designed to replace approximately 60% to 70% of your pre-disability income. The intention is to provide meaningful financial support while maintaining some incentive to return to work when possible.

Own-Occupation vs. Any-Occupation Definition of Disability

This distinction is critically important and often misunderstood:

- Own-occupation: You’re considered disabled if you cannot perform the specific duties of your own occupation — even if you could work in a different field. This definition offers broader, more favorable protection.

- Any-occupation: You’re only considered disabled if you cannot perform the duties of any occupation for which you’re reasonably qualified. This is a much higher bar to meet, and claims can be more difficult to qualify for.

Non-Cancelable and Guaranteed Renewable Provisions

These provisions protect your policy over the long term:

- Non-cancelable: The insurer cannot cancel your policy, raise your premiums, or change your benefits as long as you pay your premiums on time.

- Guaranteed renewable: You have the right to renew your policy each year, though the insurer may be able to adjust premiums for an entire class of policyholders.

At Akston Insurance, we believe that an informed consumer is a protected consumer. Understanding these terms before you sign is one of the most powerful steps you can take toward building a truly secure financial foundation.

Employer-Provided vs. Individual Disability Insurance: What You Should Know

Many employees are fortunate enough to receive group disability insurance through their workplace as part of a benefits package. While this coverage is certainly valuable — and often provided at little or no cost to the employee — it’s important to understand its limitations before assuming you’re fully protected. Comparing employer-provided coverage with individual disability insurance can help you make a more informed decision about your financial safety net.

Employer-sponsored group disability plans typically come with several notable restrictions:

- Partial income replacement: Most group plans cover only around 60% of your base salary, meaning bonuses, commissions, and other variable income are generally excluded from the calculation.

- Taxable benefits: If your employer pays the premiums on your behalf, the disability benefits you receive are typically considered taxable income — reducing your effective payout when you need it most.

- Coverage tied to employment: Group disability insurance is not portable. If you leave your job, are laid off, or change careers, your coverage ends with your employment.

- Less favorable disability definitions: Many group policies use an

How to Choose the Right Disability Insurance Coverage for Your Situation

Selecting the right disability insurance coverage isn’t a one-size-fits-all decision. Your ideal policy depends on a combination of personal finances, career, and lifestyle factors. Working through the following steps can help you make a more informed choice before speaking with a licensed insurance advisor.

Start by understanding your income replacement needs. Add up your essential monthly expenses — housing, utilities, groceries, loan payments, and healthcare — and compare that total to your take-home pay. Most financial professionals suggest that a disability policy should replace at least 60% to 70% of your pre-disability income. This calculation becomes the foundation of how much coverage you should seek.

Next, assess how long your savings could support you. If you have three to six months of expenses set aside, you may be comfortable with a longer elimination period — the waiting time before benefits begin. For most people, an elimination period of 60 to 90 days strikes a practical balance between affordability and financial security. A shorter elimination period generally means higher premiums, while a longer one lowers your cost but requires more robust savings to bridge the gap.

Consider the key factors that shape your coverage needs:

- Occupation risk level: Physically demanding jobs typically carry a higher risk of disability, which can influence both the type of policy available to you and its cost.

- Existing employer coverage: Review any group disability benefits already provided by your employer, as these may partially fulfill your needs — or leave significant gaps.

- Policy definitions: Look for an “own occupation” definition of disability, which pays benefits if you cannot perform the specific duties of your current profession, even if you could work in another capacity.

- Benefit period: A benefit period extending to age 65 or 67 offers the most comprehensive long-term protection for working-age individuals.

- Cost-of-living adjustment (COLA) rider: If your budget allows, adding a COLA rider helps your benefits keep pace with inflation over a long claim period.

It’s also worth understanding what government programs may or may not provide. Social Security Disability Insurance (SSDI) exists as a safety net, but qualifying is notoriously difficult, and benefit amounts are often insufficient to maintain your standard of living on their own.

Because disability insurance coverage involves many moving parts, working with a licensed insurance advisor is one of the most valuable steps you can take. An experienced professional can help you compare policy language, match coverage to your specific occupation and budget, and avoid common gaps that leave policyholders underprotected when they need help most.

Common Mistakes People Make When Buying Disability Insurance

Disability insurance is one of the most important financial safety nets you can have, yet many people purchase it without fully understanding what they’re buying — or they put it off until it’s too late to get the best coverage. At Akston Insurance, we want to help you avoid the pitfalls that can leave you underprotected when you need help the most.

Here are five of the most common mistakes people make when buying disability insurance:

- Relying solely on employer-provided coverage. Many people assume their workplace group disability plan is enough. However, employer-sponsored policies often replace only 50–60% of your base salary, may not be portable if you change jobs, and can have significant limitations on benefit duration. It’s worth reviewing what your employer actually provides and considering a supplemental individual policy to fill the gaps.

- Choosing a policy based on price without understanding the occupation definition. “Any occupation” policies are typically cheaper, but they only pay benefits if you cannot perform any job — not just your own profession. An “own occupation” policy offers stronger protection, particularly for skilled professionals. Understanding this distinction before you buy can make a substantial difference if you ever need to file a claim.

- Selecting too long an elimination period to reduce premiums. Opting for a 180-day or longer elimination period can lower your costs, but only if you have sufficient savings to cover your expenses during that waiting window. Without an adequate emergency fund, a long elimination period can create serious financial strain before benefits even begin.

- Underestimating how much income needs to be replaced. Many applicants base their coverage only on their base salary, forgetting to account for bonuses, commissions, or business income. Make sure your policy reflects your true earnings picture.

- Waiting until a health condition develops. Disability insurance is underwritten based on your health at the time of application. Waiting until you have a diagnosed condition can result in higher premiums, policy exclusions, or an outright denial of coverage.

Taking the time to review your needs carefully — and working with a knowledgeable advisor — can help ensure you have the right protection in place before you ever need it.

Final Thoughts: Protecting Your Income Before You Need To

Disability is far more common than most people anticipate. According to the Social Security Administration, a significant portion of working Americans will experience a disabling condition at some point during their careers — yet many remain without adequate income protection. The Council for Disability Awareness reinforces this reality, offering data that underscores just how important it is to plan ahead.

As we’ve explored throughout this guide, both short-term and long-term disability coverage serve distinct and complementary roles. Understanding key policy terms — including elimination periods, benefit durations, and definition of disability — can make a meaningful difference in whether a policy truly meets your needs when the time comes. It’s also worth remembering that employer-sponsored group coverage, while valuable, may not provide sufficient protection on its own.

Planning for disability doesn’t happen in isolation, either. If you’re thinking about comprehensive income and lifestyle protection, you may also want to explore options like long-term care insurance as part of your broader financial safety net.

Taking time now to review your current coverage — before a disability occurs — is one of the most proactive steps you can take. The team at Akston Insurance is available to help you evaluate your existing policies and explore options that may better align with your needs. Reach out to a licensed insurance advisor to start the conversation today.