Planning for the future means thinking about more than just retirement savings and life insurance. As people live longer, the chances of needing help with everyday activities — like bathing, dressing, or managing medications — continue to rise. That’s where long-term care insurance comes in. This type of coverage is designed to help pay for services that standard health insurance and Medicare typically don’t cover. Whether care is provided at home, in an assisted living facility, or in a nursing home, long-term care insurance can help protect your savings and reduce the financial burden on your family. In this guide, we’ll break down what long-term care insurance actually covers, who it’s best suited for, and how to decide if it makes sense for your situation.

What Is Long-Term Care Insurance?

Long-term care insurance is a type of coverage designed to help pay for the ongoing assistance people may need when they can no longer perform everyday activities on their own. This isn’t about recovering from a short illness or a brief hospital stay — it’s about the extended, often day-to-day support that becomes necessary due to aging, a chronic condition, a disability, or cognitive decline such as Alzheimer’s disease.

Standard health insurance and Medicare were built to cover acute medical care — things like surgeries, doctor visits, and short-term rehabilitation. What they typically don’t cover is the kind of long-term, hands-on assistance that many people eventually need just to get through their daily routines. That’s precisely the gap long-term care insurance is designed to fill.

What Does Long-Term Care Insurance Cover?

Policies can vary, but long-term care insurance generally helps cover a range of care settings and services, including:

- Home care: Personal care aides or home health workers who assist with daily tasks in your own home.

- Assisted living facilities: Residential communities that provide help with daily activities while allowing a degree of independence.

- Nursing home care: Full-time skilled or custodial care in a licensed facility.

- Adult day care: Supervised daytime programs that offer social activities and health monitoring outside the home.

What It Does NOT Cover

It’s equally important to understand the limits. Long-term care insurance is not designed to cover:

- Acute medical care, such as hospitalizations or surgeries

- Physician or specialist visits covered by health insurance

- Prescription medications (covered separately through health or Medicare Part D plans)

A practical example: Imagine Margaret, a 78-year-old retired teacher who suffered a mild stroke. After a short hospital stay covered by Medicare, she now needs help bathing, dressing, and preparing meals at home. Her long-term care insurance policy steps in to cover the cost of a home health aide five days a week — expenses her Medicare and health insurance won’t touch.

Who Needs Long-Term Care Insurance?

One of the most common misconceptions about long-term care insurance is that it’s only for the very elderly. In reality, the best time to think about this coverage is well before you actually need it — typically in your 50s or early 60s, when you’re still healthy enough to qualify and premiums are more affordable.

According to the U.S. Department of Health and Human Services, approximately 70% of people turning 65 today will need some form of long-term care during their lifetime. That’s not a small risk — it’s a near-certainty for the majority of Americans entering retirement.

People Who Should Seriously Consider LTC Insurance

- Those approaching retirement (ages 50–65): This is the sweet spot for applying. You’re likely still healthy, premiums are lower, and you have time to build up coverage before you need it.

- People with a family history of chronic illness: Conditions like Alzheimer’s, Parkinson’s, or diabetes increase the likelihood of needing extended care.

- Those without substantial savings: Without a significant financial cushion, even a few years of care costs can wipe out a lifetime of savings.

- Individuals who don’t want to burden family members: Many people underestimate how much informal caregiving falls on adult children or spouses. LTC insurance can relieve that pressure.

- Single individuals: Without a spouse or partner to lean on for informal care, single people may face higher out-of-pocket care costs and fewer support options.

Timing Matters

Long-term care insurance requires medical underwriting, which means you must apply while you’re still in reasonably good health. Waiting until you’ve been diagnosed with a serious condition can make it difficult — or impossible — to get coverage. The earlier you apply, the more options you’ll have and the lower your premiums are likely to be.

What Long-Term Care Insurance Typically Covers

Understanding the specific services covered by a long-term care insurance policy can help you determine whether a given plan meets your needs. While policies vary by carrier and plan design, most cover the following care settings and services:

- Home health care: Assistance provided by licensed aides or nurses in your own home, including help with bathing, dressing, meal preparation, and medication reminders.

- Assisted living facilities: Residential communities that provide personal care, meals, and social activities while allowing residents to maintain a level of independence.

- Nursing home care: Both skilled nursing care (medically supervised) and custodial care (help with daily activities) in a licensed facility.

- Adult day services: Structured daytime programs that provide supervision, health monitoring, and social engagement for individuals who live at home but need daytime support.

- Memory care: Specialized facilities or units designed for individuals with Alzheimer’s disease or other forms of dementia.

- Hospice support coordination: Some policies include coverage for hospice-related services that fall outside what Medicare covers.

What Triggers Your Benefits: Activities of Daily Living (ADLs)

Most long-term care insurance policies use a specific standard to determine when you’re eligible to start receiving benefits. That standard is based on your ability to perform Activities of Daily Living (ADLs) — the basic self-care tasks most of us do without thinking:

- Eating

- Bathing

- Dressing

- Toileting

- Transferring (moving from a bed to a chair, for example)

- Continence

Most policies require that you be unable to perform at least two of these six ADLs before benefits kick in. Cognitive impairment — such as Alzheimer’s disease — is often listed as a separate qualifying trigger, even if you can still perform the ADLs physically.

How Long-Term Care Insurance Policies Work

Getting familiar with how long-term care insurance policies are structured will help you make smarter comparisons when shopping for coverage. Here are the key features to understand:

Elimination Period

Think of the elimination period as a deductible measured in time rather than dollars. It’s the number of days you must pay for care out of pocket before your insurance benefits begin. Common elimination periods are 30, 60, or 90 days. A longer elimination period typically means lower premiums — but it also means more upfront costs if you need care.

Benefit Amount

Policies pay a daily or monthly benefit amount toward covered care expenses. You choose this amount when you buy the policy, often based on the typical cost of care in your area. If your actual care costs exceed the benefit, you pay the difference.

Benefit Period

This is how long your policy will pay benefits. Common options include 2 years, 3 years, 5 years, or a lifetime (unlimited) benefit period. The average long-term care need lasts about 3 years, though some conditions — particularly dementia — can require care for much longer.

Inflation Protection

Care costs rise over time, so many policies offer an inflation protection rider that increases your benefit amount each year — typically by 3% or 5% compounded annually. This feature is especially important if you’re buying coverage in your 50s and don’t expect to use it for another 20 or 30 years.

Traditional vs. Hybrid Policies

Traditional long-term care insurance pays benefits only if you need care. If you never need care, the premiums are not returned. Hybrid policies — which combine life insurance or an annuity with a long-term care rider — have become increasingly popular because they offer a death benefit or return of premium if the LTC benefit is never used. Premiums for some policies may also be tax-deductible; see IRS Publication 502 for guidance on qualified LTC insurance deductions.

The Real Cost of Long-Term Care

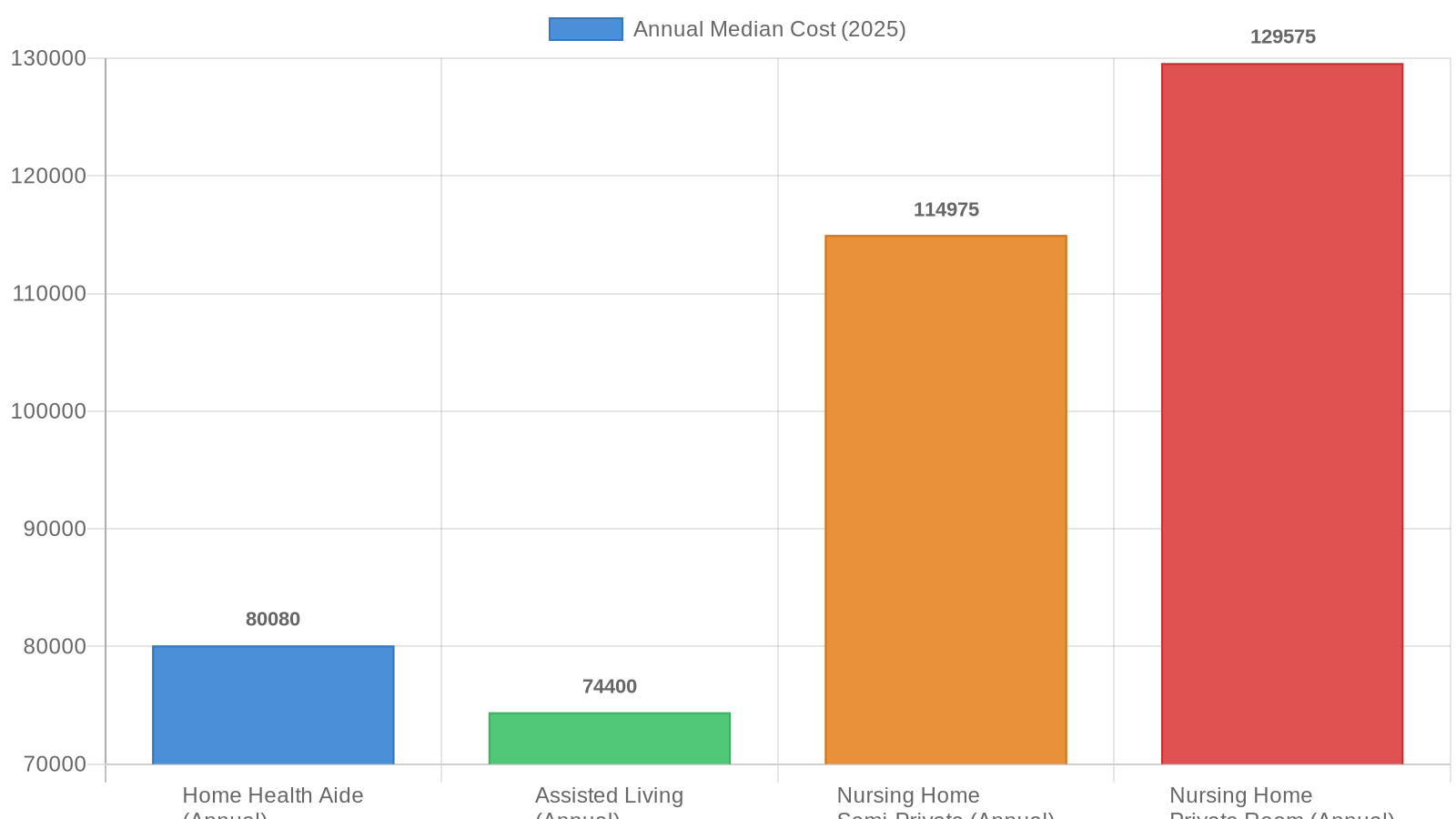

One of the most eye-opening aspects of planning for long-term care insurance is understanding just how expensive extended care can be without coverage. According to the 2025 CareScout Cost of Care Report, national median annual costs are:

- Home health aide: Approximately $80,080 per year

- Assisted living facility: Approximately $74,400 per year

- Nursing home (semi-private room): Approximately $114,975 per year

- Nursing home (private room): Approximately $129,575 per year

What Medicare Does — and Doesn’t — Cover

Many people assume Medicare will cover their long-term care needs. It won’t — at least not in any meaningful way. Medicare covers up to 100 days of skilled nursing facility care following a qualifying hospital stay, and only under specific conditions. It does not cover ongoing custodial care — the type of care most people actually need long-term.

For more information, visit Medicare.gov: Long-Term Care Coverage.

What About Medicaid?

Medicaid does cover long-term care, but only after you’ve spent down most of your assets to meet eligibility requirements. For many middle-class families, this means depleting savings, selling assets, and potentially leaving a surviving spouse with very limited resources. Long-term care insurance is one of the most effective tools for protecting assets from this outcome.

What to Look for When Buying Long-Term Care Insurance

Shopping for long-term care insurance requires careful evaluation. Here are the key factors to consider:

- Financial strength of the carrier: Look for insurers with strong ratings from agencies like AM Best or Moody’s. You want a company that will still be financially sound decades from now when you need to make a claim.

- Inflation protection: Especially important if you’re buying in your 50s. A 3% or 5% compound inflation rider helps ensure your benefit keeps pace with rising care costs.

- Elimination period: Choose a period that balances your ability to self-fund short-term care costs with the desire to keep premiums manageable.

- Benefit triggers: Confirm exactly what conditions must be met for benefits to begin — specifically which ADLs and whether cognitive impairment is covered.

- Policy portability: Make sure the coverage follows you regardless of where you receive care or where you live.

- Premium stability history: Ask about the carrier’s history of premium increases. Some insurers have raised rates significantly over the years; others have not.

Apply Early

Applying in your 50s offers two major advantages: lower premiums and a better chance of qualifying medically. Waiting until your late 60s or 70s means higher costs and a greater likelihood of being declined due to health conditions.

Working with an independent insurance advisor — someone who can compare options across multiple carriers — is one of the best ways to find a policy that fits your needs and budget. For an overview of your consumer rights and policy options, review the NAIC Long-Term Care Insurance Consumer Guide.

Planning Ahead: Your Next Steps

The reality is that most Americans will need some form of extended care during their lifetime — and the cost of that care is significant. Long-term care insurance is not a product everyone needs in the same form, but for many people, it represents one of the most important pieces of a sound retirement plan. The goal isn’t just to protect your savings — it’s to preserve your independence, protect your family, and ensure you have access to quality care when and where you need it.

Long-term care planning doesn’t exist in a vacuum. It fits alongside other key financial protection strategies, including life insurance as a retirement income strategy and disability insurance coverage — all of which work together to help you and your family weather life’s unexpected challenges.

The best time to start that conversation is before you need care, not after. If you’re in your 50s or 60s, or even if you’re approaching retirement and haven’t yet looked at long-term care options, now is the right time to take action.

Reach out to Akston Insurance today to speak with an experienced advisor who can help you understand your options, compare coverage, and build a plan that fits your life and budget.