Running a business means wearing a lot of hats — CEO, accountant, marketer, IT department, and occasionally the person who fixes the office printer. But one hat that often gets overlooked is that of risk manager. Thoughtful business owner insurance planning is one of the most important steps an entrepreneur can take to protect everything they’ve worked hard to build. Unlike employees who typically receive benefits through their employer, business owners are responsible for arranging their own coverage — from health insurance to liability protection to planning for the unexpected. That’s a lot of responsibility sitting on one (very busy) head.

This article breaks down the key areas of insurance that every business owner should understand. We’ll cover why your needs differ from a traditional employee, which types of coverage tend to matter most, how to think about protecting both your business and your personal finances, and what questions to ask when evaluating your options. Whether you’re just starting out or have been in business for years, there’s a good chance your insurance strategy could use a second look.

Why Business Owners Have Unique Insurance Needs

Running your own business is one of the most rewarding things you can do. You set your own hours, build something from the ground up, and answer to yourself. But there’s a trade-off that doesn’t always make the highlight reel: when you’re the boss, you’re also the one carrying all the risk.

Employees have it a little easier in this department. They show up, do their jobs, and go home knowing their employer handles workers’ comp, often contributes to health coverage, and manages a whole layer of liability they never have to think about. Business owners don’t get that luxury. You’re responsible for protecting yourself and your business — and those are two very different sets of problems.

This dual exposure is exactly what makes business owner insurance planning so different from standard personal insurance. A salaried employee might need a solid health plan and a term life policy. A business owner needs all of that, plus coverage for what happens if a client sues, a key employee gets injured, or the business itself has to shut down temporarily. The risk profile is simply more complex.

Think about it this way: if you slip a disc and can’t work for six months, an employee might collect short-term disability benefits through their employer. You, on the other hand, might watch your income drop to zero while your business expenses keep running like clockwork. That’s a scenario that catches a lot of entrepreneurs off guard.

There are several risks that business owners face that most employees never have to consider:

- Loss of personal income — No work often means no pay, with no employer-sponsored safety net to catch you.

- Personal liability exposure — Depending on your business structure, your personal assets could be at risk if your business is sued.

- Business continuity threats — A fire, a lawsuit, or a key person leaving can threaten the survival of the entire operation.

- Health coverage gaps — Without an employer plan, you’re responsible for finding and funding your own health insurance.

- Retirement and estate planning complexity — Your business may be your biggest asset, which creates unique planning challenges down the road.

According to the U.S. Small Business Administration, small businesses make up the vast majority of American employers — which means millions of people are navigating these risks every single day. The good news is that with the right planning, most of these exposures are very manageable. That’s exactly what we’re here to help you understand.

Life Insurance: Protecting What You’ve Built

When most people think about life insurance, they picture protecting a spouse or children from financial hardship. And that’s absolutely valid. But for business owners, life insurance does something more — it protects the business itself. Smart business owner insurance planning almost always includes a life insurance strategy, and for good reason.

Term vs. Permanent Life Insurance

The first decision most business owners face is choosing between term life insurance and permanent life insurance. Here’s a quick breakdown:

- Term life insurance provides coverage for a set period — typically 10, 20, or 30 years. It’s generally more affordable and works well for covering specific business obligations, like a loan or a startup’s early growth phase.

- Permanent life insurance (such as whole or universal life) lasts your entire lifetime and often builds cash value over time. It can serve as both a protection tool and a long-term financial asset for business owners with more complex needs.

Neither option is universally “better.” The right choice depends on your goals, your business structure, and your personal financial picture. For a deeper look at how life insurance fits into your overall planning, check out our guide on life insurance planning for families.

Key Person Life Insurance: Protecting the Irreplaceable

What would happen to your business if you — or a critical partner, top salesperson, or lead developer — were suddenly gone? That’s the question key person life insurance is designed to answer.

A key person policy is owned by the business, which also pays the premiums and receives the death benefit if a covered individual passes away. Those funds can help the company cover lost revenue, recruit and train a replacement, or simply keep the lights on during a turbulent transition. It’s not a morbid topic — it’s a practical one.

Funding Buy-Sell Agreements

If you have business partners, a buy-sell agreement is one of the most important legal documents you can have — and life insurance is often the funding mechanism behind it. Here’s how it typically works: each partner takes out a life insurance policy on the others. If one partner dies, the death benefit provides the surviving partners with the cash needed to purchase the deceased partner’s ownership share from their estate.

Without this funding in place, surviving partners might be forced to work alongside a deceased partner’s heirs — or scramble to raise capital at the worst possible time. A properly funded buy-sell agreement helps prevent that scenario entirely.

As the U.S. Small Business Administration notes, planning for business continuity is one of the most overlooked steps in small business ownership. Life insurance can be a cornerstone of that plan.

Disability Insurance: The Coverage Most Business Owners Skip

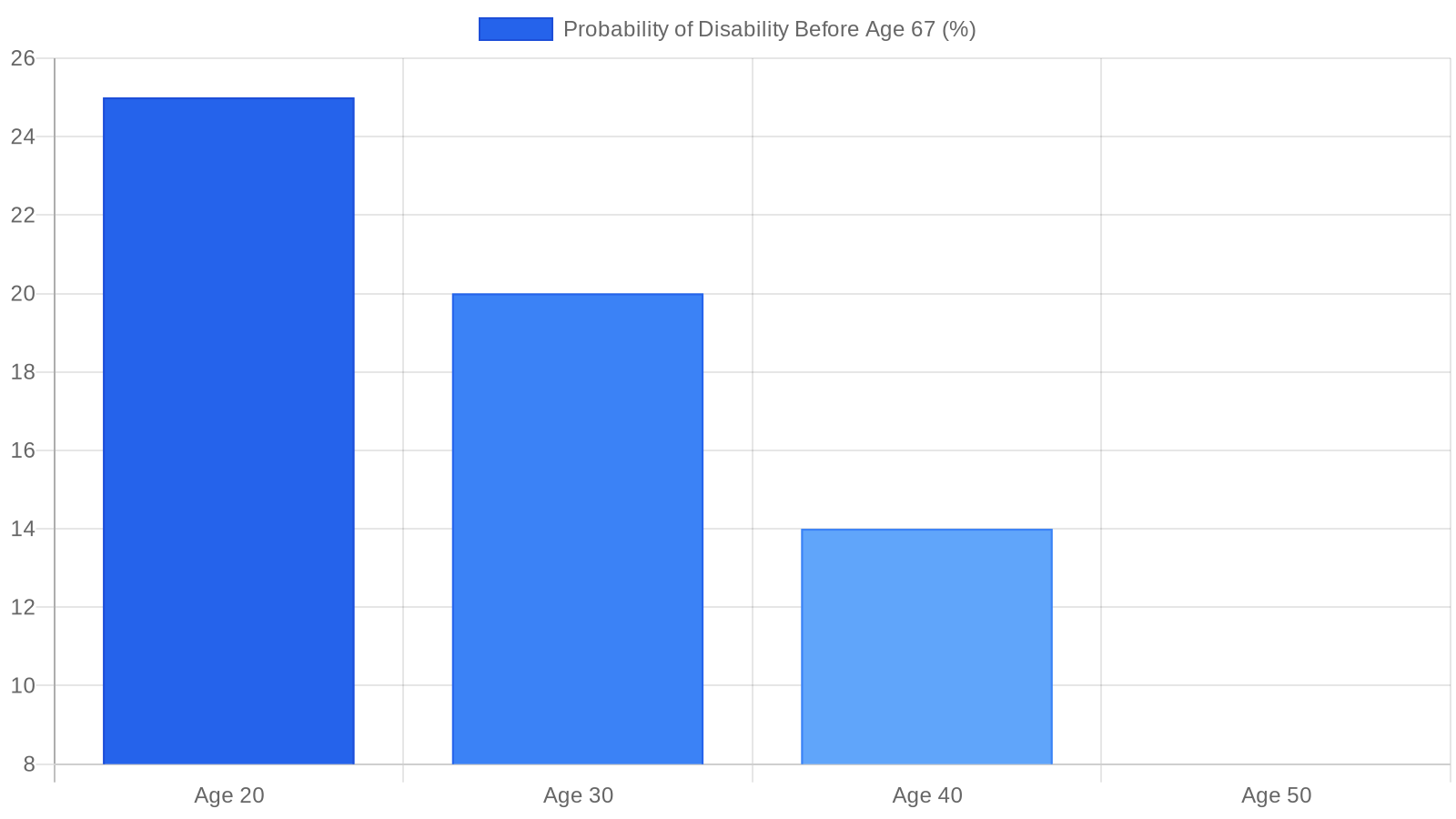

Here’s a sobering thought: according to the Social Security Administration, a disability is statistically more likely to interrupt your working years than death. Yet disability insurance remains one of the most overlooked pieces of business owner insurance planning. Most people buy life insurance without a second thought — but far fewer protect the income they depend on right now, while they’re still very much alive and working.

When you work for an employer, you might have access to short-term and long-term disability coverage as part of your benefits package. As a business owner, that safety net simply doesn’t exist unless you build it yourself. If a serious illness or injury keeps you from working for months — or longer — your business doesn’t pause along with you. Rent, utilities, payroll, and loan payments keep showing up whether you’re at your desk or not.

What Is Business Overhead Expense (BOE) Insurance?

This is where a lesser-known but incredibly valuable policy comes in: Business Overhead Expense (BOE) insurance. A BOE policy is specifically designed to cover your business’s fixed operating costs if you become disabled and can’t work. Think of it as a financial bridge that keeps the lights on while you recover.

Typically, BOE policies can help cover expenses like:

- Employee salaries and payroll taxes

- Office or storefront rent and lease payments

- Business loan installments

- Utility bills and routine operating costs

- Professional fees such as accounting or legal services

BOE coverage works alongside a personal disability income policy — one replaces your personal income, the other keeps your business afloat. Together, they give you breathing room to focus on getting better rather than watching your business unravel.

Don’t Forget Personal Disability Income Coverage

Beyond protecting the business itself, you need to protect your own paycheck. A personal disability income policy replaces a portion of your pre-disability earnings if you can’t perform your occupation due to injury or illness. For entrepreneurs whose income fluctuates, proper policy design matters a great deal — and getting that right is exactly where working with a knowledgeable advisor pays off.

To understand how these policies work and what to look for in a plan, explore our detailed guide on disability insurance benefits. It’s one of the smartest steps any business owner can take as part of a complete business owner insurance planning strategy.

Business Liability and Property: Don’t Overlook the Basics

When most people think about insurance for their business, they picture something going wrong — a lawsuit, a fire, a customer slipping on a wet floor. And honestly, that instinct is right. These are exactly the kinds of risks that solid business owner insurance planning is designed to address. The good news is that the building blocks of business protection are well-established and relatively straightforward to understand.

Let’s walk through the core types of business insurance that most entrepreneurs should at least consider.

General Liability Insurance

This is the foundation for most businesses. General liability insurance helps protect your business if someone claims you caused bodily injury, property damage, or personal harm — like a client who trips in your office or a contractor who accidentally damages a customer’s home. It’s often required by landlords, vendors, and larger clients before they’ll even sign a contract with you. Think of it as your business’s handshake with the outside world.

Professional Liability (Errors & Omissions)

If your business provides a service or professional advice — consulting, design, IT, accounting, and many others — general liability alone may not be enough. Professional liability insurance, often called Errors & Omissions (E&O), helps protect you if a client claims your work caused them financial harm. Even well-intentioned professionals make mistakes, and a single dispute can become expensive fast.

Commercial Property Insurance

Whether you own your building or rent a workspace, commercial property insurance helps protect your physical assets — equipment, inventory, furniture, and more — from risks like fire, theft, and certain weather events. If your business couldn’t operate without its physical space or tools, this coverage deserves serious attention.

The Business Owner’s Policy (BOP): A Bundled Option

For many small businesses, a Business Owner’s Policy (BOP) offers an efficient way to combine general liability and commercial property coverage into one package — often at a lower cost than purchasing each separately. It’s designed with small and mid-sized businesses in mind, though eligibility varies by industry and business size.

Here’s a quick summary of common business insurance coverage types worth exploring:

- General Liability Insurance — Covers third-party bodily injury and property damage claims

- Professional Liability (E&O) — Protects against claims of negligence or mistakes in professional services

- Commercial Property Insurance — Covers physical business assets from covered perils

- Business Owner’s Policy (BOP) — Bundles general liability and property coverage for eligible small businesses

- Workers’ Compensation — Required in most states if you have employees; covers work-related injuries

- Commercial Auto Insurance — Covers vehicles used for business purposes

- Cyber Liability Insurance — Increasingly important for businesses that handle sensitive customer data

Not every business needs every type of coverage, and the right mix depends on your industry, size, and risk exposure. The U.S. Small Business Administration offers helpful guidance on understanding business insurance requirements and options.

At Akston Insurance, we help business owners cut through the noise and evaluate which coverages actually make sense for their situation — without the pressure or the jargon. A little clarity now can prevent a very costly surprise later.

Group Benefits: Competing for Talent as a Small Business

Here’s a truth that every small business owner eventually faces: you can’t always out-pay a large corporation. But you can out-benefit one — or at least get closer than you might think. A well-rounded group benefits package is one of the most powerful tools in your business owner insurance planning toolkit, and it does double duty by protecting your team while also making your business more attractive to top talent.

When job seekers compare offers, they’re not just looking at salary. Health coverage, dental, vision, and retirement options are often just as important — sometimes more so. Offering these benefits signals that you’re a serious employer who invests in the people who help build your business.

What a Competitive Benefits Package Looks Like

For most small businesses, a strong benefits package typically includes some combination of the following:

- Group health insurance: The cornerstone of most employee benefits programs. Even offering a modest contribution toward premiums can set you apart from competitors who offer nothing.

- Dental and vision coverage: Often overlooked, but highly valued by employees — especially families. These plans are generally affordable to add and easy to administer.

- Group life and disability insurance: Basic coverage at low group rates adds meaningful protection for your team without a heavy cost burden on your business.

- Retirement plans: A SIMPLE IRA or SEP-IRA can be a cost-effective way to offer retirement benefits, even if you’re running a lean operation.

Section 125 Cafeteria Plans and Tax Advantages

One often-underused strategy is the Section 125 cafeteria plan, which allows employees to pay their share of insurance premiums with pre-tax dollars. This reduces their taxable income — and it reduces your payroll tax liability at the same time. It’s a genuine win-win that many small businesses simply haven’t set up yet.

If your business has fewer than 25 full-time equivalent employees, you may also qualify for the Small Business Health Care Tax Credit through the IRS, which can offset a portion of what you spend on employee health premiums. It’s worth reviewing with a qualified tax professional.

To explore your coverage options in more detail, take a look at our guide to group health insurance for small businesses. Understanding what’s available is the first step toward building a benefits strategy that works for your budget and your team.

The bottom line? Smart benefit offerings aren’t just a perk — they’re part of a broader business owner insurance planning approach that helps you attract, retain, and protect the people who make your business run.

How to Build a Business Owner Insurance Planning Strategy

Knowing you need insurance is one thing. Actually putting together a plan that works for your business, your employees, and your personal financial life? That’s where most entrepreneurs get stuck. The good news is that business owner insurance planning doesn’t have to be overwhelming — especially when you break it down into clear, manageable steps.

Here’s a practical five-step approach to help you get started.

- Take stock of your risks. Every business is different. A freelance graphic designer faces very different risks than a restaurant owner or a construction contractor. Start by listing the biggest threats to your business — lawsuits, property damage, a key employee getting sick, or even your own disability. This risk inventory becomes the foundation of your entire strategy.

- Identify coverage gaps. Once you know your risks, compare them against what you currently have in place. Many business owners discover they’re either underinsured in critical areas or paying for overlapping coverage they don’t need. Look at your business policies and your personal policies together — because the two are more connected than most people realize.

- Prioritize by impact. Not every risk deserves the same amount of attention. Focus first on the scenarios that would be financially catastrophic — a serious liability lawsuit, a long-term disability, or an unexpected death affecting a key partner. These are the gaps you want to close before anything else.

- Build your coverage layer by layer. Think of your insurance strategy as a stack. Start with the essentials — general liability, property, and health coverage. Then layer in more specialized protection like disability insurance, life insurance, and business continuation coverage as your budget and risk profile allow.

- Review and adjust regularly. Your business will grow, change, and face new challenges over time. A coverage plan that made sense when you had three employees may fall short when you have thirty. Set a reminder to review your policies at least once a year — and any time you hit a major business milestone.

Of course, you don’t have to figure all of this out on your own. Working with an independent insurance advisor — like the team at Akston Insurance — means you get guidance that’s tailored to your specific situation, not just a one-size-fits-all policy recommendation. An independent advisor can compare options across multiple carriers, help you spot gaps you might have missed, and make sure your business and personal coverage work together the way they should.

Building a smart strategy takes a little time upfront, but it pays off every day your business keeps running smoothly.

Putting It All Together

Running a business takes courage, creativity, and — yes — a solid insurance strategy. Throughout this article, we’ve covered a lot of ground, and here’s a quick look at what matters most.

Your business faces risks on multiple fronts: property damage, liability claims, employee health needs, and the very real possibility that you — the person driving everything — could become sick or injured. Each of these risks calls for a thoughtful, layered response. No single policy covers everything, which is exactly why business owner insurance planning requires a big-picture view rather than a quick checkbox approach.

We also explored how your personal financial life is deeply connected to your business. Life insurance and disability coverage aren’t just personal decisions — they’re business ones too. And when it comes to your team, offering group health benefits can be one of the smartest investments you make in retention and morale.

Most importantly, remember that your insurance needs will change as your business grows. A policy that fit perfectly on day one may leave major gaps by year five. Regular reviews aren’t just a good idea — they’re essential.

You don’t have to figure all of this out alone. The advisors at Akston Insurance are here to help you assess your risks, understand your options, and build a strategy that actually fits your business.